Monte Carlo Option Pricing

Finance

What you need to know first 1 concepts, 1 layers

The requisite-knowledge inventory for this page, bottom-up: the primitives at the base, combined upward until you reach what this page assumes. Skim the layers you already own; start wherever the ground gets unfamiliar.

- base

- ↳you are here

Monte Carlo simulation is a powerful numerical method for pricing options, especially when analytical solutions are not available. It works by simulating many possible future stock price paths and averaging the payoffs.

Geometric Brownian Motion

We model the stock price using geometric Brownian motion:

In the risk-neutral world, . The solution is:

For discrete time steps, we use:

where is a standard normal random variable.

Monte Carlo Method

The Monte Carlo method for option pricing:

- Simulate stock price paths to expiration

- Calculate the payoff for each path

- Average the payoffs and discount to present value

The option price is estimated as:

The standard error decreases as , so more simulations improve accuracy.

Payoff Functions

For a European call option:

For a European put option:

where is the stock price at expiration and is the strike price.

Python Implementation

The following code implements Monte Carlo option pricing:

import numpy as np

import matplotlib.pyplot as plt

import matplotlib as mpl

from scipy.stats import norm

def set_publication_style():

"""Set publication-quality matplotlib style."""

mpl.rcParams.update({

'font.family': 'serif',

'font.size': 12,

'axes.labelsize': 14,

'axes.titlesize': 16,

'axes.linewidth': 1.2,

'axes.labelpad': 8,

'axes.titlepad': 10,

'xtick.labelsize': 12,

'ytick.labelsize': 12,

'xtick.direction': 'in',

'ytick.direction': 'in',

'xtick.top': True,

'ytick.right': True,

'xtick.major.size': 6,

'ytick.major.size': 6,

'xtick.major.width': 1.2,

'ytick.major.width': 1.2,

'legend.fontsize': 12,

'legend.frameon': False,

'lines.linewidth': 2,

'lines.markersize': 6,

'figure.dpi': 100,

'savefig.dpi': 300,

'savefig.bbox': 'tight'

})

set_publication_style()

def black_scholes(S, K, T, r, sigma, option_type='call'):

"""Black-Scholes analytical formula for comparison."""

d1 = (np.log(S / K) + (r + 0.5 * sigma**2) * T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

if option_type == 'call':

return S * norm.cdf(d1) - K * np.exp(-r * T) * norm.cdf(d2)

else:

return K * np.exp(-r * T) * norm.cdf(-d2) - S * norm.cdf(-d1)

def monte_carlo_option_price(S0, K, T, r, sigma, n_simulations, option_type='call', n_steps=1):

"""

Price European option using Monte Carlo simulation.

Parameters

----------

S0 : float

Initial stock price

K : float

Strike price

T : float

Time to expiration (years)

r : float

Risk-free rate

sigma : float

Volatility

n_simulations : int

Number of Monte Carlo simulations

option_type : str

'call' or 'put'

n_steps : int

Number of time steps (1 for simple simulation)

Returns

-------

tuple

Option price, standard error, payoffs array

"""

np.random.seed(42) # For reproducibility

dt = T / n_steps

# Simulate stock prices

if n_steps == 1:

# Simple one-step simulation

Z = np.random.normal(0, 1, n_simulations)

ST = S0 * np.exp((r - 0.5 * sigma**2) * T + sigma * np.sqrt(T) * Z)

else:

# Multi-step simulation

ST = np.zeros(n_simulations)

S = np.full(n_simulations, S0)

for _ in range(n_steps):

Z = np.random.normal(0, 1, n_simulations)

S *= np.exp((r - 0.5 * sigma**2) * dt + sigma * np.sqrt(dt) * Z)

ST = S

# Calculate payoffs

if option_type == 'call':

payoffs = np.maximum(ST - K, 0)

else:

payoffs = np.maximum(K - ST, 0)

# Discount to present value and calculate statistics

option_price = np.exp(-r * T) * np.mean(payoffs)

standard_error = np.exp(-r * T) * np.std(payoffs) / np.sqrt(n_simulations)

return option_price, standard_error, payoffs

def simulate_stock_paths(S0, mu, sigma, T, dt, n_paths):

"""

Simulate multiple stock price paths using geometric Brownian motion.

Parameters

----------

S0 : float

Initial stock price

mu : float

Drift (expected return)

sigma : float

Volatility

T : float

Total time

dt : float

Time step

n_paths : int

Number of paths to simulate

Returns

-------

ndarray

Array of stock price paths

"""

n_steps = int(T / dt)

paths = np.zeros((n_paths, n_steps + 1))

paths[:, 0] = S0

for i in range(1, n_steps + 1):

Z = np.random.normal(0, 1, n_paths)

paths[:, i] = paths[:, i-1] * np.exp((mu - 0.5 * sigma**2) * dt + sigma * np.sqrt(dt) * Z)

return paths

# Parameters

S0 = 100 # Initial stock price

K = 100 # Strike price

T = 1.0 # Time to expiration (1 year)

r = 0.05 # Risk-free rate (5%)

sigma = 0.2 # Volatility (20%)

n_simulations = 100000 # Number of Monte Carlo simulations

# Calculate option prices

call_price_mc, call_se, call_payoffs = monte_carlo_option_price(

S0, K, T, r, sigma, n_simulations, 'call'

)

put_price_mc, put_se, put_payoffs = monte_carlo_option_price(

S0, K, T, r, sigma, n_simulations, 'put'

)

# Compare with Black-Scholes

call_price_bs = black_scholes(S0, K, T, r, sigma, 'call')

put_price_bs = black_scholes(S0, K, T, r, sigma, 'put')

print("Monte Carlo Option Pricing Results:")

print("\nCall Option:")

print(" Monte Carlo: {:.4f} ± {:.4f}".format(call_price_mc, call_se))

print(" Black-Scholes: {:.4f}".format(call_price_bs))

print(" Difference: {:.4f}".format(abs(call_price_mc - call_price_bs)))

print(" Relative Error: {:.2f}%".format(100*abs(call_price_mc - call_price_bs)/call_price_bs))

print("\nPut Option:")

print(" Monte Carlo: {:.4f} ± {:.4f}".format(put_price_mc, put_se))

print(" Black-Scholes: {:.4f}".format(put_price_bs))

print(" Difference: {:.4f}".format(abs(put_price_mc - put_price_bs)))

print(" Relative Error: {:.2f}%".format(100*abs(put_price_mc - put_price_bs)/put_price_bs))

# Plot 1: Simulated stock price paths

n_paths_plot = 20

dt = 1/252 # Daily steps

paths = simulate_stock_paths(S0, r, sigma, T, dt, n_paths_plot)

time = np.linspace(0, T, paths.shape[1])

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Top left: Stock price paths

axes[0, 0].plot(time, paths.T, alpha=0.6, linewidth=0.5)

axes[0, 0].axhline(K, color='r', linestyle='--', linewidth=2, label='Strike Price')

axes[0, 0].set_xlabel('Time (years)')

axes[0, 0].set_ylabel('Stock Price')

axes[0, 0].set_title('Simulated Stock Price Paths')

axes[0, 0].legend()

axes[0, 0].grid(True, alpha=0.3)

# Top right: Payoff distribution (call)

axes[0, 1].hist(np.exp(-r*T) * call_payoffs, bins=50, alpha=0.7, edgecolor='black')

axes[0, 1].axvline(call_price_mc, color='r', linestyle='--', linewidth=2, label='Mean: {:.2f}'.format(call_price_mc))

axes[0, 1].axvline(call_price_bs, color='g', linestyle='--', linewidth=2, label='BS: {:.2f}'.format(call_price_bs))

axes[0, 1].set_xlabel('Discounted Payoff')

axes[0, 1].set_ylabel('Frequency')

axes[0, 1].set_title('Call Option Payoff Distribution')

axes[0, 1].legend()

axes[0, 1].grid(True, alpha=0.3)

# Bottom left: Payoff distribution (put)

axes[1, 0].hist(np.exp(-r*T) * put_payoffs, bins=50, alpha=0.7, edgecolor='black', color='orange')

axes[1, 0].axvline(put_price_mc, color='r', linestyle='--', linewidth=2, label='Mean: {:.2f}'.format(put_price_mc))

axes[1, 0].axvline(put_price_bs, color='g', linestyle='--', linewidth=2, label='BS: {:.2f}'.format(put_price_bs))

axes[1, 0].set_xlabel('Discounted Payoff')

axes[1, 0].set_ylabel('Frequency')

axes[1, 0].set_title('Put Option Payoff Distribution')

axes[1, 0].legend()

axes[1, 0].grid(True, alpha=0.3)

# Bottom right: Convergence analysis

n_sims_range = [1000, 5000, 10000, 50000, 100000, 500000]

call_prices_conv = []

put_prices_conv = []

for n in n_sims_range:

call_p, _, _ = monte_carlo_option_price(S0, K, T, r, sigma, n, 'call')

put_p, _, _ = monte_carlo_option_price(S0, K, T, r, sigma, n, 'put')

call_prices_conv.append(call_p)

put_prices_conv.append(put_p)

axes[1, 1].semilogx(n_sims_range, call_prices_conv, 'b-o', label='Call (MC)')

axes[1, 1].semilogx(n_sims_range, put_prices_conv, 'r-o', label='Put (MC)')

axes[1, 1].axhline(call_price_bs, color='b', linestyle='--', alpha=0.5, label='Call (BS)')

axes[1, 1].axhline(put_price_bs, color='r', linestyle='--', alpha=0.5, label='Put (BS)')

axes[1, 1].set_xlabel('Number of Simulations')

axes[1, 1].set_ylabel('Option Price')

axes[1, 1].set_title('Monte Carlo Convergence')

axes[1, 1].legend()

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('figures/monte_carlo_options_plot.png', dpi=300, bbox_inches='tight')

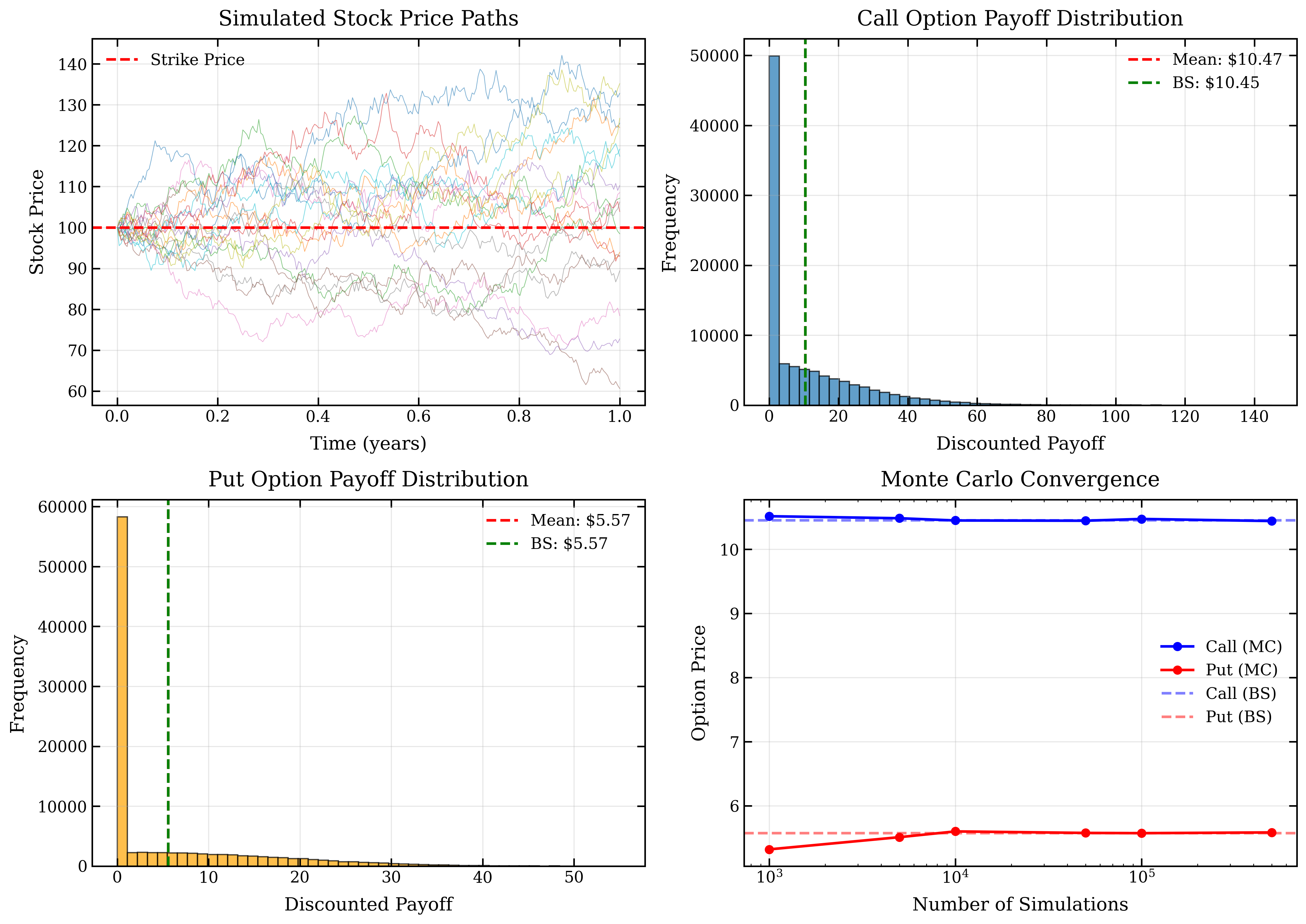

plt.show()Visualization

The following plots show simulated stock price paths, payoff distributions, and convergence analysis:

Advantages

Monte Carlo simulation offers several advantages:

- Flexibility: Can handle complex payoffs and path-dependent options

- Multi-dimensional: Easy to extend to multiple assets

- Stochastic volatility: Can incorporate time-varying volatility

- American options: Can price early exercise using least squares Monte Carlo

- Intuitive: Direct simulation of the underlying process

Variance Reduction

Several techniques can reduce the variance of Monte Carlo estimates:

- Antithetic variates: Use along with

- Control variates: Use known analytical solutions

- Importance sampling: Change the probability measure

- Quasi-Monte Carlo: Use low-discrepancy sequences

Applications

Monte Carlo is used for:

- Exotic options (Asian, barrier, lookback)

- Basket options and correlation products

- Options with stochastic volatility

- Real options and project valuation

- Risk management and stress testing